{kind=link}

What the central bank does today can change your mortgage payment next month.

When policymakers raise or lower the policy rate, short-term benchmarks move within minutes and lenders adjust retail quotes over weeks to months.

That timing difference is why fixed and variable mortgages react very differently, and it matters for affordability, rate‑lock timing, and refinance choices.

This post explains how policy moves reach mortgage pricing, the usual lags and risks, and three practical steps to help you decide whether to lock, wait, or pick a different product.

Immediate Effects of Central Bank Policy Changes on Mortgage Choices

When a central bank moves its policy rate, borrowing costs shift almost immediately in market pricing, then trickle down to the rate your lender actually quotes a few weeks later. A hike pushes costs higher because banks pay more to fund loans and investors want better yields to hold mortgage debt. A cut lowers funding costs and usually brings mortgage rates down, though how much depends on what’s happening with inflation expectations, credit conditions, and how fast lenders want to adjust their own pricing. The Federal Reserve raised rates 11 times between early 2022 and the end of 2023, the most aggressive campaign in nearly 40 years. By August 2024, the average 30‑year fixed mortgage rate had dropped to 6.35% from a peak of 7.79% in late October 2023 as markets started pricing in expected cuts.

The lag between a policy announcement and the actual rate change on your mortgage offer varies. Market benchmark rates—overnight funding costs, Treasury yields, mortgage‑backed security spreads—reprice within minutes of a central bank statement. But retail mortgage pricing takes longer. Lenders need to watch secondary‑market movements, check credit spreads, and adjust their own funding mixes. Variable‑rate mortgages tied to short‑term benchmarks typically adjust within zero to three months after a policy move. Fixed‑rate mortgages react to long‑term yields, which shift based on inflation expectations and what the central bank is doing with quantitative easing or tightening programs. Fixed‑rate pricing changes can show up within days but often take weeks to months to settle. Full system‑wide credit effects may need six to 24 months to work through bank balance sheets.

Fixed and variable mortgages respond differently because they’re priced from different benchmarks. Variable loans follow short‑term policy‑linked rates like the federal funds rate, SOFR, or SONIA, and they capture nearly the full pass‑through of a policy change within weeks. Fixed loans are built on long‑term market yields such as the 10‑year Treasury or swap curve, plus a lender spread. These yields move when inflation or growth expectations shift, not just when the policy rate ticks up or down. That’s why a 1.00 percentage point policy hike might raise a variable rate by close to 1.00 percentage point but lift a 30‑year fixed rate by only 0.50 to 1.50 percentage points, depending on what happens to term premiums and credit spreads at the same time.

Policy‑driven changes immediately affect six core mortgage decision areas. Affordability shifts because higher rates mean larger monthly payments, while lower rates free up purchasing power or reduce refinancing costs. Rate locks become a timing game: when the central bank signals further hikes, locking sooner protects against rising quotes. Expected cuts favor waiting or using float‑down clauses. Refinance timing opens up during a policy‑cut cycle as rates fall. Hikers shrink refinance volume and push borrowers to consider cash‑out or term shortening instead. Product choice gets trickier during tightening because risk‑averse borrowers lean toward fixed products for payment certainty. Easing can make variable products attractive if cuts are credible and you can tolerate volatility. Payment risk rises when policy‑rate increases raise the chance of payment shock on adjustable loans. Cuts reduce it and can make hybrid ARMs competitive again. Qualification gets tighter or looser depending on the direction: rising rates lower maximum loan amounts under debt‑to‑income constraints, and falling rates expand buying power and make marginal borrowers eligible.

Consolidated Transmission Channels From Policy Rate to Mortgage Pricing

Central bank policy touches mortgage pricing through four main channels: the short‑term policy rate, quantitative programs, market expectations, and credit spreads. When a central bank raises or lowers its policy rate—the federal funds rate, Bank Rate, deposit rate, or cash rate—it directly changes the cost of overnight borrowing for commercial banks. Banks fund some portion of their mortgage lending from short‑term wholesale markets, so a higher policy rate raises their marginal cost of funds. That cost increase gets passed to borrowers, especially on variable‑rate or adjustable‑rate mortgages priced from short‑term benchmarks like SOFR, SONIA, or EURIBOR. Variable mortgage pricing is typically the benchmark rate plus a lender margin of 100 to 300 basis points. If the benchmark jumps by 1.00 percentage point, the retail variable rate usually moves 0.50 to 1.00 percentage point within zero to three months, with the rest of the spread absorbed or passed depending on competition and credit conditions.

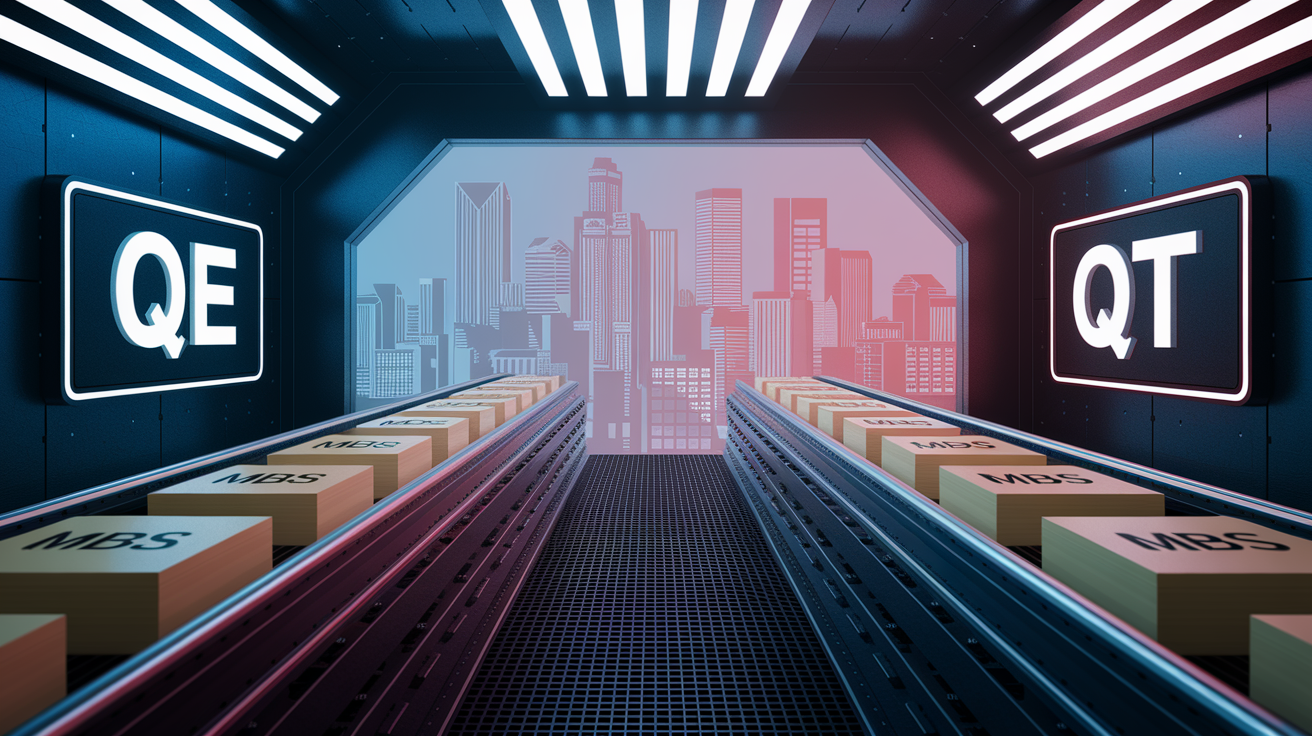

Fixed‑rate mortgages follow a different path. They’re priced from long‑term market yields, usually a government bond yield or interest‑rate swap curve, plus a lender spread of 100 to 300 basis points. A policy‑rate increase can push long‑term yields higher if it signals future inflation or credible tightening, but the effect is partial and depends on inflation expectations and term premiums. Quantitative easing (QE) programs, where central banks buy government bonds or mortgage‑backed securities, reduce the supply of those bonds and push yields down by 20 to 150 basis points, depending on program size and market conditions. Quantitative tightening (QT) reverses that effect. The central bank shrinks its balance sheet, bond supply increases, and long‑term yields rise. QT also tightens bank funding conditions because it drains reserves, raising funding costs and widening credit spreads.

| Channel | Mechanism | Impact on Mortgages |

|---|---|---|

| Policy rate (short‑term) | Central bank sets overnight rate → short‑term benchmark moves → bank funding costs shift | Variable rates adjust quickly (0–3 months); fixed rates may shift if expectations for inflation or future policy change long‑term yields |

| Quantitative easing / tightening | Bond purchases reduce supply and lower yields; balance‑sheet runoff increases supply and raises yields | QE lowers fixed rates 20–150 bps; QT raises them and can widen spreads if bank reserves drain |

| Market expectations | Forward guidance and inflation forecasts shift investor pricing of future policy moves | Mortgage rates move ahead of actual policy changes; lenders reprice in anticipation of hikes or cuts |

| Credit spreads and bank balance sheets | Tighter credit or reduced liquidity raises the margin lenders charge above benchmarks | Spreads can widen 50–300 bps during stress, offsetting policy easing or amplifying hikes at the retail level |

How Policy Changes Affect Fixed vs. Variable Mortgage Structures

Variable‑rate mortgages track short‑term benchmarks directly tied to the central bank’s policy rate, so they capture most of a policy change within weeks. When the policy rate rises by 1.00 percentage point, the short‑term index usually moves by close to 1.00 percentage point, and the lender’s variable‑rate product reprices by 0.50 to 1.00 percentage point within zero to three months. How much depends on margin changes and competitive pressure. Fixed‑rate mortgages are priced from long‑term government or swap yields, which shift when inflation expectations or term premiums change, not just when the policy rate ticks. A 1.00 percentage point policy hike might lift the 10‑year Treasury yield by only 0.20 to 0.80 percentage points if markets believe inflation will stay controlled or if the hike signals slower future growth. That partial transmission means a fixed‑rate mortgage might rise by 0.50 to 1.50 percentage points for the same policy move. The adjustment often takes weeks to months as long‑term yields digest the policy signal, inflation prints, and fiscal outlook.

The borrower risk profile diverges sharply between the two structures. Variable borrowers face payment volatility. A 1.00 percentage point rate increase on a $300,000, 30‑year mortgage shifts the monthly payment from approximately $1,610 at 5.00% to approximately $1,798 at 6.00%. That’s an increase of roughly $188, or 11.7%. If the central bank follows a multi‑year hiking cycle, cumulative payment increases can strain budgets and trigger defaults if income doesn’t keep pace. Fixed borrowers lock payment certainty but sacrifice the ability to benefit automatically from policy cuts. If rates fall after they lock, they must refinance to capture the lower rate, paying closing costs and resetting the loan clock. That tradeoff means fixed mortgages are favored when policy‑rate volatility is high or when long‑term yields look low relative to expected inflation. Variable products appeal when the curve is inverted and rate cuts are credible within 12 to 24 months.

Lender spread behavior also differs. On variable products, margins tend to be sticky. Lenders may raise the rate faster than they lower it, capturing asymmetric profit during a hiking cycle and delaying relief during easing. On fixed products, spreads widen or compress based on credit conditions and secondary‑market liquidity. During quantitative tightening or credit stress, mortgage‑backed security spreads can blow out by 50 to 300 basis points. That means borrowers see fixed rates rise even if policy rates hold steady. Aggressive quantitative easing compresses spreads and can deliver fixed‑rate relief beyond what the policy‑rate path alone would suggest. Understanding these dynamics helps you choose the product that matches your interest‑rate view, cash‑flow tolerance, and refinancing flexibility.

Timeline and Lag Effects When Central Banks Shift Policy

The journey from policy announcement to a new mortgage rate on your closing documents unfolds in stages, each with its own timing. Markets reprice benchmark rates within minutes to hours of a central bank statement. Traders adjust positions in government bonds, interest‑rate futures, and mortgage‑backed securities as soon as the policy decision hits the wires, moving short‑term overnight rates and long‑term yields in real time. Those market moves happen fast because professional investors run scenario models and react to forward guidance, inflation forecasts, and dissent votes published alongside the rate decision. By the end of the trading day, Treasury yields, swap curves, and MBS spreads have usually absorbed the new information and settled at levels that reflect updated expectations for inflation, growth, and future policy.

Retail mortgage pricing lags behind market moves because lenders must translate benchmark shifts into posted rates, manage pipeline hedging, and adjust for credit‑risk and funding‑cost changes on their own balance sheets. Variable‑rate products reprice fastest, often within days to a few weeks, because they’re mechanically tied to short‑term benchmarks. Fixed‑rate pricing takes longer, typically weeks to a few months, as lenders watch secondary‑market activity, assess spread behavior, and lock in funding for new originations. Full system‑wide effects on credit conditions—such as tighter underwriting, reduced lending capacity, or changes in securitization demand—can take six to 24 months to materialize, especially during quantitative tightening when bank reserves drain and balance‑sheet constraints bind.

The sequence from announcement to borrower impact follows five steps. First, the central bank announcement on day zero: policy decision, statement, forward guidance, and updated forecasts get published, and a press conference provides context. Second, market benchmark adjustment happens within minutes to hours. Short‑term rates (overnight, three‑month), government bond yields, swap curves, and mortgage‑backed security spreads reprice based on the policy path implied by the announcement. Third, lender repricing occurs over days to weeks. Variable‑rate lenders update benchmark margins and post new rates. Fixed‑rate lenders adjust pricing sheets as they observe secondary‑market MBS trading levels and hedging costs. Fourth, borrower rate lock or quote surfaces over weeks to months. The new retail rates appear in rate‑lock offers, refinance quotes, and pre‑approval letters. Borrowers closing within 30 to 60 days see the updated pricing. Fifth, credit‑condition effects unfold over months to two years. Banks adjust underwriting standards, lending volumes shift, securitization markets reprice risk, and the full macroeconomic feedback loop (inflation, employment, housing demand) influences long‑term equilibrium mortgage rates.

Mortgage Decision Strategies Under Tightening or Easing Cycles

When the central bank is raising rates, affordability shrinks fast and you face a narrowing window to lock favorable pricing. The Federal Reserve’s 11 rate increases between early 2022 and the end of 2023 pushed the average 30‑year fixed mortgage rate from historic lows to a peak of 7.79% in late October 2023, choking refinance volumes and forcing buyers to compete with higher monthly payments. During a tightening cycle, fixed‑rate mortgages become more attractive because they cap payment risk, even though the initial rate may be higher than a variable product. Locking early is usually the safer choice when the central bank signals more hikes ahead and inflation prints run hot, because waiting exposes you to repricing risk and shrinking purchasing power. Refinancing during a hiking cycle makes sense only if you’re consolidating higher‑rate debt, shortening your term to save total interest, or tapping equity for an investment that beats the higher borrowing cost.

When the central bank pivots to cutting rates, affordability improves and refinancing windows reopen. By August 2024, the average 30‑year fixed rate had fallen to 6.35% as markets priced in expected cuts totaling roughly 0.50 percentage points across the remaining meetings that year. A drop from 7.79% to 6.35% saves approximately $292 per month on a $300,000, 30‑year mortgage. That’s $3,504 annually. If closing costs for a refinance run $3,000, the break‑even period is roughly 10 to 11 months ($3,000 ÷ $292 ≈ 10.3 months). The simple refinance break‑even formula is: total refinance costs divided by monthly payment savings. When that number falls below your planned holding period—commonly 24 to 36 months for many borrowers—refinancing becomes a clear decision. During an easing cycle, variable‑rate products can also make sense if you expect further cuts within 12 to 24 months and can tolerate interim payment volatility. The variable rate adjusts downward automatically, capturing savings without refinance costs.

Timing a rate lock or float decision hinges on your view of the policy path and your tolerance for uncertainty. Lock when volatility is high, when forward guidance signals more tightening, or when the quoted rate meets your affordability threshold and you’re closing within 30 to 60 days. Float when the yield curve is inverted, inflation is cooling, and credible central bank communication points to near‑term cuts. Use a float‑down clause if your lender offers one, so you capture declines without losing your application slot. Product choice during a cycle depends on the same tradeoffs: fixed for payment certainty and protection against further hikes, variable for automatic benefit from cuts and lower initial rates when the curve is steep.

Lock when the central bank forward guidance implies rising rates, inflation expectations are climbing, long‑term yields are trending up, or you’re within your lock window and unwilling to gamble on timing. Float when policy‑cut expectations are credible and priced into the curve, the yield curve is inverted, and you have time before closing. Always use a float‑down option if available. Refinance when the rate drop is at least 0.75 to 1.00 percentage point, break‑even fits your holding horizon (commonly under 24 to 36 months), and closing costs are competitive. Choose variable when you expect cuts within 12 to 24 months, can handle payment volatility, and short‑term rates are materially above long‑term yields. Choose fixed when you need certainty or expect hikes or persistent inflation.

Yield Curve, Term Premiums, and Mortgage Pricing Implications

The yield curve, the relationship between short‑term and long‑term interest rates, shapes fixed‑mortgage pricing more directly than the policy rate itself. When the curve steepens (long‑term yields rise faster than short‑term rates), fixed mortgage rates climb because lenders price from the 10‑year Treasury or swap curve plus a spread. A steepening curve often signals expectations of future inflation or stronger growth, pushing term premiums higher and making long‑term borrowing more expensive. When the curve flattens or inverts (short‑term rates meet or exceed long‑term rates), fixed mortgage rates can stay stable or even fall despite policy‑rate hikes, because investors price in future rate cuts or slower growth. An inverted curve typically favors fixed‑rate borrowing over variable, because you lock a relatively low long‑term rate while short‑term rates sit elevated and are expected to decline.

Term premiums, the extra yield investors demand for holding long‑term bonds instead of rolling over short‑term securities, compress during quantitative easing and expand during quantitative tightening. When the central bank buys large volumes of long‑term bonds, it reduces the supply available to private investors, lowering yields and narrowing the term premium. That compression can cut fixed mortgage rates by 20 to 150 basis points, depending on the scale of asset purchases and market conditions. When quantitative tightening begins and the central bank’s balance sheet shrinks, bond supply increases, term premiums widen, and fixed rates rise even if the policy rate holds steady. Credit stress adds another layer. During financial turmoil, mortgage‑backed security spreads can blow out by 50 to 300 basis points as liquidity dries up and investors flee to safer government bonds, pushing retail mortgage rates well above what the policy rate or Treasury yield alone would predict.

| Yield Curve Scenario | Effect on Fixed Rates | Borrower Implication |

|---|---|---|

| Steepening (long‑term yields rise faster than short‑term) | Fixed mortgage rates climb as term premium and inflation expectations increase | Lock fixed rates quickly if buying; variable products may offer lower initial payments but carry refinance or rollover risk |

| Flattening (long‑term yields fall relative to short‑term) | Fixed rates stabilize or drop; spread to variable narrows | Fixed becomes more attractive for payment certainty; variable loses relative advantage |

| Inversion (short‑term yields exceed long‑term) | Fixed rates may be lower than variable despite policy tightening; term premium compressed or negative | Lock fixed for cheap long‑term funding; wait for policy cuts if choosing variable; inversion often precedes recession and eventual rate cuts |

How Quantitative Easing and Tightening Alter Mortgage Availability and Pricing

Quantitative easing increases central bank demand for mortgage‑backed securities and government bonds, pushing prices up and yields down. When the Federal Reserve or another central bank buys MBS in the secondary market, it absorbs supply that would otherwise be held by pension funds, insurers, and other investors, reducing the yield those securities offer and lowering the benchmark rate lenders use to price new fixed mortgages. Historical QE programs have reduced long‑term yields by 20 to 150 basis points, depending on program size, duration, and market conditions at the time. Lower yields translate into lower fixed mortgage rates for borrowers, expanding affordability and refinancing volumes. QE also signals that the central bank expects low inflation and weak growth for an extended period, which reinforces downward pressure on long‑term yields and keeps mortgage rates low even as short‑term policy rates remain near zero.

Quantitative tightening reverses those effects. The central bank stops reinvesting maturing bonds, allowing its balance sheet to shrink and increasing the supply of bonds and MBS in the market. That higher supply pushes prices down and yields up, raising the benchmark lenders use for fixed‑rate pricing. QT also drains reserves from the banking system, tightening funding conditions and raising the cost of short‑term wholesale borrowing. Banks respond by widening credit spreads, tightening underwriting standards, and reducing the volume of new mortgage originations. The combined effect can lift fixed mortgage rates by tens to hundreds of basis points and reduce mortgage availability, especially for marginal borrowers or non‑conforming loan products. Borrowers feel QT through higher rates, stricter qualification, and less competitive secondary‑market pricing, making it harder to refinance or purchase compared to the QE environment that preceded it.

Borrower Tools and Calculators for Policy‑Driven Mortgage Scenarios

Three calculators give you the numbers you need to make policy‑informed mortgage decisions: a monthly payment calculator, a refinance break‑even calculator, and a rate‑sensitivity slider. The monthly payment calculator uses the formula M = P × rmonthly × (1 + rmonthly)^n / ((1 + rmonthly)^n − 1), where P is principal, rmonthly is the annual interest rate divided by 12, and n is the total number of monthly payments. For example, a $300,000 loan at 5.00% annual interest over 30 years gives r_monthly = 0.05 / 12 = 0.0041667 and n = 360, producing M ≈ $1,610.46. If the rate rises to 6.00%, M ≈ $1,798.65, an increase of roughly $188 per month, or 11.7%. Running this calculation at your current rate, an expected rate after central bank cuts, and a stress rate if hikes continue shows you the payment range and helps size the loan you can afford under different policy scenarios.

Monthly payment calculator: input principal, annual percentage rate, and term in months. Output is the fixed monthly payment. Run scenarios at current rate, expected cut rate (e.g., minus 0.50%), and stress hike rate (e.g., plus 0.50%). Refinance break‑even calculator: input total closing costs and the difference between old and new monthly payments. Output is the number of months to recoup costs. Refinancing makes sense when break‑even is shorter than your holding period. Rate‑sensitivity slider: adjust the rate in 25‑basis‑point or 100‑basis‑point increments and watch the monthly payment change. Helps visualize the cost of waiting or locking at different points in a policy cycle. Timeline projection tool: plot your expected closing date against the central bank’s meeting calendar and forward guidance. Decide whether to lock now or float through the next policy decision.

The output from these tools tells you whether a rate move materially changes your decision. If a 0.25 percentage point cut saves you only $40 per month but locking costs you 0.10 percentage point in extra spread for a 60‑day window, the net benefit is small and you may choose to lock. If a 0.50 percentage point cut saves $100 per month and forward guidance credibly points to that cut within 60 days, floating with a rate‑lock backup makes sense. Always compare the dollar impact of rate changes to your budget constraints, opportunity cost of waiting, and risk tolerance for payment volatility.

How Central Bank Communication Shapes Borrower Expectations

Central banks manage market expectations through forward guidance, explicit statements about the likely path of future policy rates, and regular publication of meeting minutes, economic forecasts, and inflation targets. When a central bank signals that rates will remain higher for longer, long‑term yields typically rise as investors price persistent inflation or delayed cuts, pushing fixed mortgage rates up even before the next policy meeting. When forward guidance shifts to acknowledge cooling inflation or rising unemployment, long‑term yields fall and mortgage rates decline in anticipation of cuts, often weeks or months before the actual policy move. That pre‑pricing means borrowers who wait for the official cut may find that mortgage rates have already adjusted, capturing much of the expected benefit and leaving little room for further declines unless the central bank surprises with deeper or faster easing.

Credibility matters. A central bank with a strong track record of hitting its inflation target and following through on guidance will see markets move smoothly in response to its statements, minimizing volatility and giving borrowers clearer signals for timing locks and refinances. A central bank that flip‑flops or misses forecasts injects uncertainty, widening mortgage‑rate spreads as lenders price a risk premium for unpredictability. You benefit from monitoring the central bank’s communication calendar: major policy meetings, chair speeches, quarterly forecasts, and minutes releases. These events trigger benchmark‑rate moves that flow into mortgage pricing within days.

Forward guidance on the policy‑rate path matters most. Explicit language like “rates will remain restrictive” or “cuts are likely in coming months” shifts long‑term yield expectations and mortgage‑rate trends. Inflation‑target updates and progress reports tell you whether inflation is cooling toward the 2% target, which supports expectations for cuts. Persistent overshoots delay easing and keep rates elevated. Labor‑market assessments reveal whether strong employment data can delay cuts and push mortgage rates higher, or whether rising unemployment accelerates easing expectations and lowers rates. Quarterly economic forecasts and dot plots give markets a roadmap. Central bank staff projections for growth, inflation, and the policy rate get priced into mortgage markets immediately. Meeting minutes and dissent votes reveal internal debate and uncertainty. Dissent votes signal policy risk and can widen mortgage spreads if markets fear abrupt shifts.

FAQs on Central Bank Policies and Mortgage Decisions

Do central bank rate hikes immediately raise my mortgage rate? Not one‑to‑one and not immediately. Variable‑rate mortgages adjust within zero to three months, capturing most of a short‑term benchmark move. Fixed‑rate mortgages follow long‑term yields, which shift based on inflation expectations and term premiums. A 1.00 percentage point policy hike might raise fixed rates by 0.50 to 1.50 percentage points over weeks to months. Retail pricing lags market moves by days to weeks as lenders reprice.

How much can a central bank rate cut save me each month? A rate drop from 7.79% to 6.35% on a $300,000, 30‑year mortgage saves approximately $292 per month, or $3,504 annually. The exact savings depend on your loan size, term, and the magnitude of the rate change. Use the payment formula to run your own scenario. Even a 0.25 percentage point drop can save $40 to $50 per month on a typical loan.

When should I refinance during a rate‑cut cycle? Refinance when the rate drop is at least 0.75 to 1.00 percentage point, closing costs are reasonable (commonly $2,000 to $5,000), and the break‑even period (costs ÷ monthly savings) is shorter than your holding horizon. A common rule is break‑even under 24 to 36 months. If you plan to move or pay off the loan sooner, a higher rate drop is needed to justify the cost.

Should I lock my rate now or wait for the next central bank meeting? Lock now if you’re closing within 30 to 60 days, volatility is high, or forward guidance signals more hikes. Float if credible guidance points to cuts within your lock window, the yield curve is inverted, and you have a float‑down option. Timing risk is real. Markets often price cuts ahead of the announcement, so waiting may not deliver additional savings.

How does quantitative easing help mortgage borrowers? QE lowers long‑term yields by 20 to 150 basis points by increasing central bank demand for bonds and mortgage‑backed securities. Lower yields reduce fixed mortgage rates, improve affordability, and expand refinancing opportunities. QE also signals low inflation and weak growth expectations, reinforcing downward pressure on rates. The effect reverses during quantitative tightening, when yields rise and mortgage rates climb.

What happens to mortgage rates if inflation stays high despite rate hikes? Persistent inflation keeps long‑term yields elevated because investors demand higher compensation for erosion of purchasing power. Fixed mortgage rates remain high or rise further, even if the central bank pauses hikes, because term premiums expand and credit spreads widen. Variable rates track short‑term policy moves, so they may stabilize if the central bank stops hiking. But affordability stays compressed until inflation cools and yields fall.

Final Words

Policy moves change borrowing costs now: variable rates can shift in weeks, while fixed rates track long-term yields and often take months to move. That timing matters for affordability, rate locks, and refinance timing.

Use the calculators and scenario checks described above, and watch spreads and the yield curve. If you run a couple of quick scenarios, understanding how changes in central bank policy affect mortgage decisions will help you pick the safer path and act with more confidence.

FAQ

Q: What is the 3 7 3 rule in mortgage?

A: The 3 7 3 rule in mortgage isn’t a universal standard; some lenders or advisers use it as a quick affordability or reserve guideline, but meanings vary—always ask your lender what they mean before acting.

Q: Will changing banks affect me getting a mortgage?

A: Changing banks can affect getting a mortgage because lenders review account history, direct deposits, and asset trails. Keep 2–3 months of statements, explain big transfers, and avoid switching just before applying.

Q: What is the biggest factor affecting mortgage approval?

A: The biggest factor affecting mortgage approval is your debt-to-income ratio (how much of your monthly income goes to debt payments). Lenders use it to judge repayment ability; aim for under about 43%.

Q: Will mortgage rates drop if the Fed cuts rates?

A: Mortgage rates may fall if the Fed cuts, but not automatically. Variable rates usually pass through within 0–3 months; fixed rates follow long-term yields and can take weeks–months and only partially move.